Apartment investors rushed to take out more loans than ever in 2021. Lenders think they were only getting warmed up for 2022.

By: Bendix Anderson

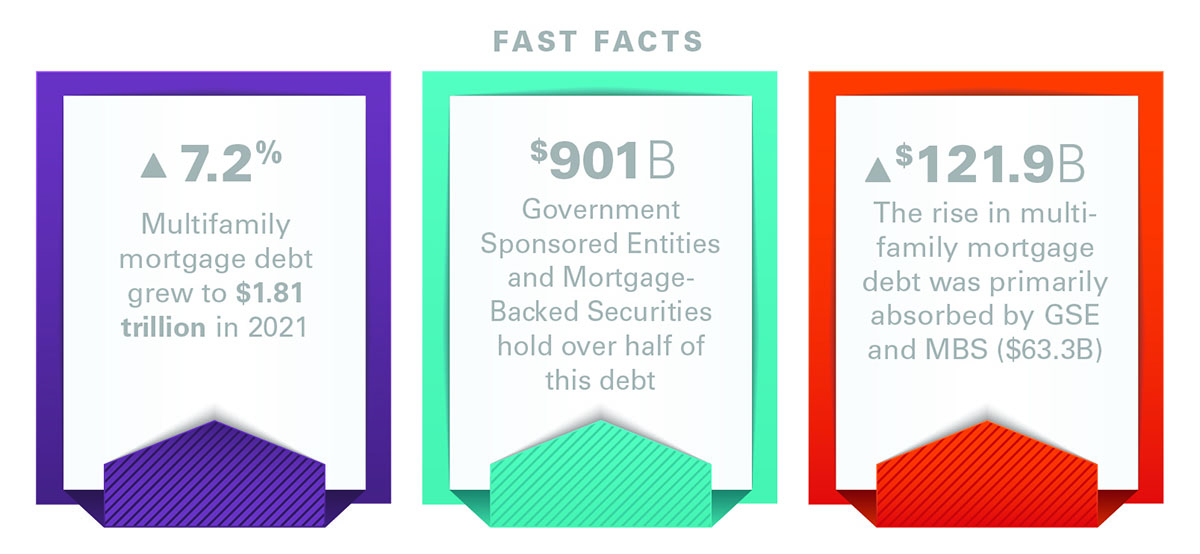

Apartment investors are taking out more loans than ever. In 2021, they rushed to get loans to buy new apartment properties and refinance the debt on existing properties.

Investors spent more to buy apartment properties at the end of 2021 than ever before. They spent more than $80 billion in December 2021, which is roughly twice what they spent to buy apartment properties the month before, according to Real Capital Analytics (RCA) based in New York City. These sales are much more than apartment investors spent during the worst of the pandemic—often less than $10 billion a month.

The dollars investors spent in 2021 are also many times what multifamily investors spent before the pandemic. Their usual monthly totals in 2018 and 2019—which seemed like busy years at the time—often hovered below $20 billion, according to RCA.

They are likely to take out even more loans in 2022.

“Expectations for 2022 are very, very strong,” said Jamie Woodwell, vice president of commercial real estate research for the Mortgage Bankers Association (MBA). “There is a strong appetite from borrowers and lenders to make loans.”

More than half (63 percent) of commercial and multifamily lenders expect the total market originations to increase 5 percent or more in 2022, according to MBA’s 2022 Commercial Real Estate Finance (CREF) Outlook Survey. Nearly three-quarters of the lenders surveyed (74 percent) expect their own originations to increase by 5 percent or more.

The boom in lending is fueled by borrowers are still eager to refinance their loans on apartment properties while interest rates are still low, and by a growing number of investors who want to borrow money to buy apartment properties.

Rise of debt funds

These investors need a huge amount of financing to complete their deals. Relatively new lenders are expanding their businesses just in time to provide this financing, including debt funds created by private equity fund managers.

“There are 100 or more debt funds that are actively lending,” said Patrick McGlohn, senior managing director for the mortgage banking platform at Berkadia, working in the firm’s office in Washington, D.C. “On any given deal there could be 30 or more debt funds that fit the opportunity profile.”

Debt funds have become more important to real estate borrowers. “Investor-driven lenders” including debt funds lent close to twice (up 77 percent) as much money to commercial and multifamily properties in the fourth quarter of 2021 as they had in the same period in 2018, according to MBA.

The loans provided by debt funds often have relatively short, five-year terms and interest rates that float over a benchmark, short-term interest rate like the Secured Overnight Financing Rate (SOFR). That’s very different than the long-term, fixed-rate loans many apartment buyers once relied on.

“Fixed-rate, long-term debt is really out of vogue,” said Kelli Carhart, senior managing director and head of multifamily debt production for CBRE. Today, many apartment borrowers prefer “permanent” loans with shorter terms than the traditional seven or ten years —they value the flexibility to sell earlier without having to pay a pre-payment penalty.

The interest rates offered by debt funds have also become much more competitive. Some offer rates floating 150 basis points over SOFR—compared to spreads as high as 500 basis point a few years ago, experts say.

A few also offer choices including longer-term, fixed-rate financing, which has been unusual for debt funds. “There are debt funds today that are offering fixed rate loans for as much as ten years,” says Dave Borsos, vice president of capital markets for the National Multifamily Housing Council (NMHC).

Freddie, Fannie focus on workforce

Many apartment borrowers still rely on the loan programs of Freddie Mac and Fannie Mae for financing—though less so than in the recent past. Until very recently, the two mortgage giants originated as much as half of the apartment loans in any given year.

“Agency lenders were hard to beat for the last few years for the combination of leverage and pricing,” said Eric McGlynn, managing director for the capital markets group at Walker & Dunlop, which is the largest lender in Fannie Mae’s Delegated Underwriting and Servicing (DUS) program for multifamily properties.

Freddie Mac and Fannie Mae lenders are still likely to lend more money to apartment properties in 2022 than ever before. The officials at the Federal Housing Finance Agency (FHFA) who oversee Freddie Mac and Fannie Mae have increased the dollar volume of apartment loans they are allowed to purchase to $78 billion each, up from $70 billion each in 2021.

That increase is not nearly enough to keep up with the increase in demand for loans from apartment properties.

The federal officials at FHFA also directed Freddie Mac and Fannie Mae to focus on financing workforce housing. At least half of the multifamily loans bought by the government-sponsored enterprises in 2022 must be to communities with rents affordable to low- and moderate-income households. At least 25 percent of the loans must be to properties with rents affordable to households earning up to 60 percent of the area median income.

To satisfy FHFA’s requirements, Freddie Mac and Fannie Mae offer lower interest rates to properties with more affordable rents—often dozens of basis points less than their usual fixed interest rates.

“The agencies are more competitive for assets that qualify as workforce housing,” said CBRE’s Carhart.

Freddie Mac and Fannie Mae already lend billions of dollars each year to government-subsidized affordable housing through initiatives like Freddie Mac’s Tax-Exempt Loan (TEL) program, which provides large, permanent mortgages with preferential interest rates to housing developments subsidized with tax-exempt bond financing and federal low-income housing tax credits.

Agency lenders now also offer preferential interest rates to apartments where the rents are low enough to be affordable to moderate-income people—often simply because the properties are older.

To get these low interest rates, the owners of these “naturally occurring affordable housing” properties are often willing to commit to keep the rents affordable, even though the properties receive no other affordable housing subsides.

In November 2021, Walker & Dunlop closed a $124 million Fannie Mae mortgage to The Avanti, a property with 930 apartments that first opened in 1965 in District Heights, Maryland. The new owners received a low interest rate in exchange for agreeing to keep the rents at a certain number of the apartments affordable to low and moderate-income households.

“We see the agencies moving towards a more mission-driven, affordable housing focus,” said McGlohn.

Freddie Mac and Fannie Mae loans can technically be as large as 80 percent of the value of an apartment property. That’s significantly more leverage than the limits set by banks and life company lenders, which often cover about 55 percent of 60 percent of the value of a property.

But high-prices and rising-interest rates are forcing Freddie Mac and Fannie Mae to constrain the size of their loans relative to the income produced by an apartment property. Most agency loans made today are equal to less than 65 percent the likely sale price of the property, says CBRE’s Carhart.

That’s because the agencies typically require borrowers to show that their properties produce income equal to 1.25x the likely debt service payments of a loan. That requirement is constraining the size of the loans offered by Freddie Mac and Fannie Mae as the prices investors are willing to pay for apartment properties keep getting higher relative to the income produced at the properties.

Rising prices for apartment properties and rising interest rates have given other lenders like debt funds and life company lenders a new advantage in the competition to make loans to more expensive, Class-A apartments.

Apartment buyers paid prices that worked out to an average capitalization rate of less than 5 percent in January 2022. That’s down sharply from roughly 5.5 percent in 2020, according to RCA.

Investors are often willing to pay high prices relative to the proven income from an apartment property because they believe they believe rents are likely to rise.

Lenders like debt funds and life companies are also somewhat more likely than Freddie Mac and Fannie Mae lenders to go along with those optimistic assumptions. “They are willing to be a little more flexible—they don’t need the current income. They are not as worried about cash flow,” said Carhart.

In contrast, Freddie Mac and Fannie Mae apartment loans are often securitized and sold to bond buyers who are concerned with the proven cash flow from the properties.

“Some lenders will base underwriting on projected cash flows and that allows them to offer more leverage,” said Rich Martinez, senior vice president of production and sales for Freddie Mac Multifamily. “Freddie Mac takes a more conservative approach, underwriting to rents in place.”

Because of their more aggressive underwriting, many debt funds are still able to offer high-leverage loans that cover 80 percent of the value of an apartment community.

Even with this new competition, many apartment borrowers who want to lock in low interest rates with long-term financing still eagerly take out loans from Freddie Mac and Fannie Mae lenders.

“Agency financing can be an attractive option for many borrowers, especially those with a longer-term hold period,” said William T. Colgan, partner with CHA Partners, a development firm based in Bloomfield, N.J.

Life cos., banks, CMBS rush to lend

Other lenders also compete fiercely to make apartment loans. “Life companies have been very aggressive to win market share on core assets,” said Colgan.

Life company lenders have a history of offering the lowest, fixed interest rates to the strongest, Class-A apartment properties. However, their loans rarely cover more than 55 or 60 percent of the value of the property.

“Life companies continue to provide aggressive pricing on lower leverage deals in strong markets,” said Newmark’s Karaffa.

A few life companies have even partnered with debt funds created by private equity giants like KKR, Apollo and Blackstone, using their capital to make more permanent loans to apartment properties.

Banks also continue to make longer-term loans to apartment properties. “Banks continue to get more aggressive to capture business by providing both construction and permanent financing,” said Karaffa.

Builders currently have 700,000 new apartments under construction—that’s the most since the 1970s, says Woodwell.

Even CMBS lenders, who never regained the prominence they had before the Global Financial Crisis, are useful to many apartment borrowers. “CMBS loans are an attractive option for locking in fixed rates,” said Colgan. “Rising interest rates are pushing borrowers towards locking in longer-term financing.”

Borrowers keep borrowing

Officials at the Federal Reserve still plan to raise their benchmark interest rates several times in 2022 to slow down rising prices. Their current plan appears to be several rates hikes, raising the Fed Funds rate from near zero to as high as 1.9 percent by the end of 2022.

War in Europe has scrambled forecasts for the World economy. Interest rates have continued to inch higher in the weeks since Russia invaded Ukraine in late February, despite the other uncertainties for the global economy created by the conflict.

The yield on 10-year U.S. Treasury bonds rose above 2.2 percent in mid-March. That’s up from roughly 1.5 percent in most of 2021, and it’s the highest the yield has been since before the pandemic.

“Some financiers have begun to reopen their spreads and tighten their leverage requirements,” said John Chang, senior vice president and national director of the Research Services Division at Marcus & Millichap. “Thus far, the movement has not been significant or broad-based, but if the war in Ukraine escalates, either militarily or through cyberattacks, lenders may adopt a more conservative posture.”

Rising interest-rates, both short-term and long-term, are likely to have a negative effect on lending in 2022, according to MBA’s survey of originators. But most still expect to make more loans this year than last year—even though last year broke records.